The Corporate Transparency Act (“CTA”) is a new federal law requiring many corporations, limited liability companies, and other registered entities to report information about their beneficial owners. The CTA takes effect on January 1, 2024. Is your business ready to comply? Let’s find out!

Background

The CTA added a new section, 31 U.S.C. 5336, to a larger body of law called the Bank Secrecy Act (“BSA”). This new Section 5336 is intended to provide the U.S. Treasury Department’s Financial Crimes and Enforcement Network (“FinCEN”) with key information for the purpose of detecting, preventing, and punishing terrorism, money laundering, and other misconduct carried out through business entities. FinCEN will also permit Federal, State, Local, and Tribal government officials, and certain foreign officials upon request through a Federal government agency, to obtain beneficial ownership information for authorized activities related to national security, intelligence, and law enforcement.

The CTA represents the culmination of more than a decade of congressional efforts to implement beneficial ownership reporting for business entities. When fully implemented, it will create a database of beneficial ownership information (“BOI”) within FinCEN. The CTA’s reporting requirements generally apply to smaller, more lightly regulated entities that are less likely to be subject to any other BOI reporting requirements. By contrast, the CTA exempts certain categories of larger, more heavily regulated entities from its reporting requirements.

Who Needs to File a BOI Report?

FinCEN has issued Rules and Regulations as it moves toward implementing the CTA. See 31 CFR 1010. Under the CTA, ALL entities formed or registered to do business in the United States will be required to do one of the following:

- Submit a Beneficial Ownership Information Report to FinCEN; or

- Confirm qualification for one of the exemptions for the CTA’s reporting requirements.

Entities that are required to report are called “Reporting Companies.” There are two types of Reporting Companies:

- Domestic Reporting Companies are corporations, LLCs, and any other entities created by a state filing with a Secretary of State or any similar office in the United States.

- Foreign Reporting Companies are corporations, LLCs, and any other entities formed under the law of a foreign country that have registered to do business in the United States by a state filing with a Secretary of State or any similar office.

What are the BOI Report Exemptions?

If an entity is not created by such a state filing (e.g., most trusts), the entity is not subject to the BOI reporting requirements.

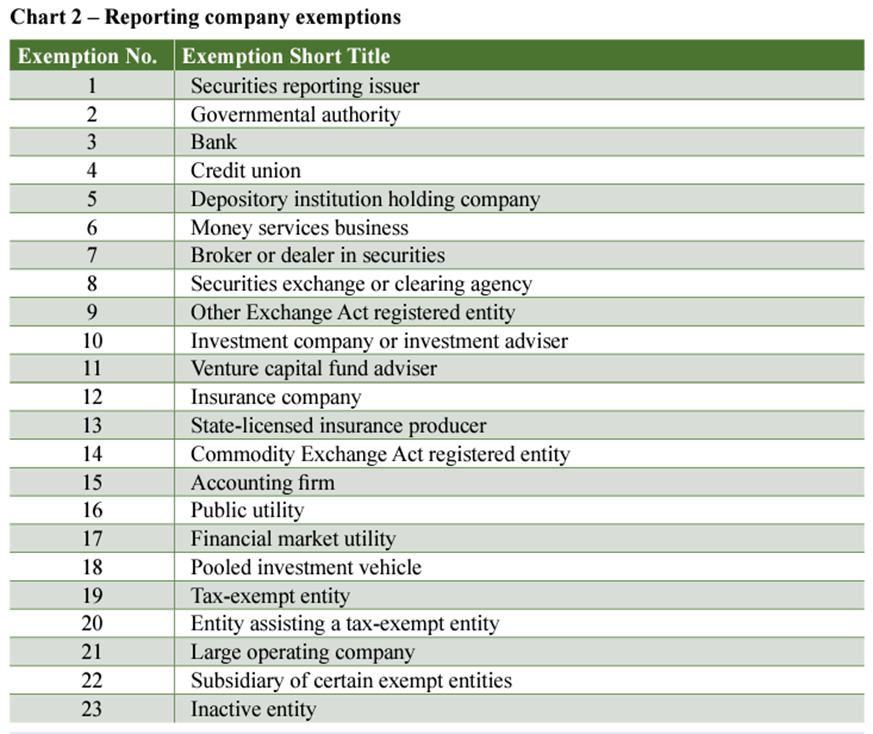

In addition, there are 23 types of entities that are exempt from the BOI reporting requirements. These entities include publicly traded companies meeting specified requirements, many nonprofits, and certain large operating companies. The general reasoning is that these types of entities are subject to additional oversight, regulation, or reporting.

Here is a chart outlining the 23 exemptions (click to enlarge). This chart is taken from FinCEN’s Small Entity Compliance Guide at Chapter 1.2 (see page 4).

When Does the BOI Report Need to be Filed?

A Reporting Company created or registered to do business before January 1, 2024, will have until January 1, 2025 (i.e., one year) to file its initial beneficial ownership information report.

A Reporting Company created or registered on or after January 1, 2024, will have 90 days to file its initial beneficial ownership information report. This 90-day deadline runs from the time the entity receives actual notice that its creation or registration is effective, or after a Secretary of State or similar office first provides public notice of its creation or registration, whichever is earlier.

What is in the BOI Report?

At the time of writing this article, the BOI Report form itself is not yet available. The report and accompanying information is set to be posted on FinCEN’s beneficial ownership information webpage, and the report will be submitted electronically. However, FinCEN will not accept reports before January 1, 2024. Until the actual form itself is available, we will not know exactly what information FinCEN is requesting.

The CTA requires Reporting Companies to file the following information:

- Full legal name

- Any tradename or D/B/A

- Address

- The State, Tribal, or Foreign Jurisdiction of formation

- Taxpayer identification number

The CTA requires Beneficial Owners and Company Applicants to file the following information:

- Full legal name

- Date of birth

- Address

- A “unique identifying number,” which means a number from a valid US passport, government ID, driver’s license, foreign passport (if none of the previous documents have been issued)

- An image of the document from which the unique identifying number was obtained

We know that FinCEN is seeking to obtain information about the individuals who actually own or control an entity and/or individuals who take the steps to create an entity. So, entities should start thinking about who these individuals are in their organizations.

The analysis will be less complicated for Reporting Companies created or registered on or after January 1, 2024. Those entities will simply need to report their Company Applicants. A company that must report its Company Applicants will have only up to two individuals who could qualify as Company Applicants, and these are:

- The individual who directly files the document that creates or registers the company; and

- If more than one person is involved in the filing, the individual who is primarily responsible for directing or controlling the filing.

For Reporting Companies created or registered before January 1, 2024, the analysis will be more complicated. As such, these entities should start thinking about and listing the individuals that could qualify as beneficial owners. A beneficial owner is an individual who either directly or indirectly:

- Exercises substantial control over the reporting company, or

- Owns or controls at least 25% of the reporting company’s ownership interests.

There are four different ways that an individual can exercise substantial control:

- The individual is a senior officer (the company’s president, chief financial officer, general counsel, chief executive office, chief operating officer, or any other officer who performs a similar function).

- The individual has authority to appoint or remove certain officers or a majority of directors (or similar body) of the Reporting Company.

- The individual is an important decision-maker for the Reporting Company.

- The individual has any other form of substantial control over the Reporting Company as explained further in FinCEN’s Small Entity Compliance Guide (see Chapter 2.1, “What is substantial control?”).

Therefore, Reporting Companies that are already established before January 1, 2024 need to determine which individuals in their organization meet the definitions and categories above. This may be a complex analysis. There are also some exceptions that may apply for certain individuals. As an example, an accountant or lawyer would usually not be considered a beneficial owner, unless they hold a position such as general counsel or something that may be considered a “senior officer” type of position.

Here is some good news for all Reporting Companies: there will not be a fee associated with filing the BOI Report.

Conclusion

As with any newer legislation, rules, or regulations, there will be a number of questions raised once the reporting process goes live. Entities that were created or registered before January 1, 2024 will have one year to comply with the reporting requirements, but now is the time to start thinking about this. Please reach out to Pat Shriver or any of the other attorneys in our Corporate and Business Practice Group to help with your analysis.

Related Attorneys